The Institute for Supply Management released its monthly manufacturing Purchasing Managers Index (PMI) on Dec. 2, reflecting November activity, which showed higher results following a decline in October.

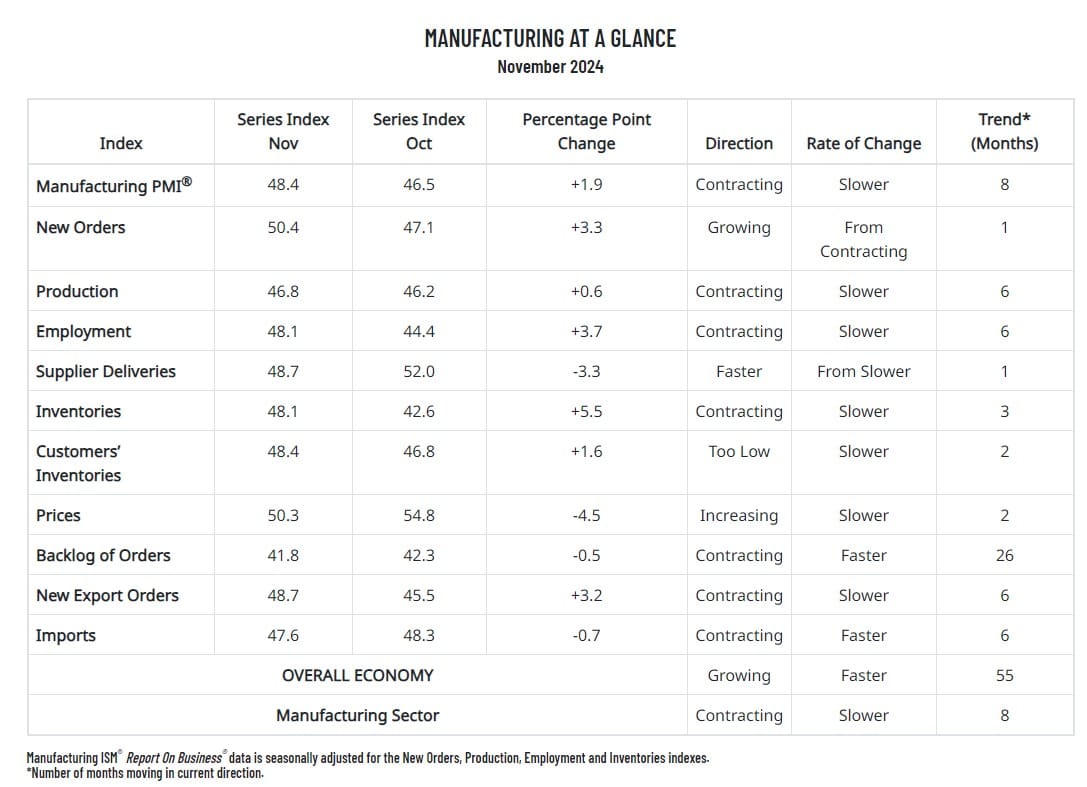

The PMI — regarded as a reliable indicator of overall U.S. industrial economic health — was up 1.9 percentage points at 48.4% from October’s 46.5%. It indicated that activity remained subdued but moderated higher during the month. More granularly, the latest report showed that demand increased with a healthy bump in new orders (into expansion territory), while production saw a modest gain and inputs stayed accommodative.

The November PMI reading indicated contraction (anything below 50.0%) for the eighth consecutive month.

Here’s how that has looked in bar chart form since December 2023.

source: tradingeconomics.com

Of the November PMI’s 10 factoring indexes, six ended the month in contraction territory. The figure was driven by declines of 4.5 in prices, 3.3 in supplier deliveries and 0.7 in imports, offset by increases of 5.5 in inventories, 3.3 in new orders and 3.2 in new export orders.

“Demand remains weak, as companies prepare plans for 2025 with the benefit of the election cycle ending,” ISM Manufacturing Business Survey Committee Chairman Timothy Fiore said in the November report. “Production execution eased in November, consistent with demand sluggishness and weak backlogs. Suppliers continue to have capacity, with lead times improving but some product shortages reappearing.”

Fiore added that 66% of manufacturing GDP contracted in November, up from 63% in October. The share of sector GDP registering a composite PMI calculation at or below 45% — considered a good barometer of overall manufacturing weakness — was 48% in November, a 2-point increase from October.

The three manufacturing industries reporting growth in November were: Food; Beverage & Tobacco Products; Computer & Electronic Products; and Electrical Equipment, Appliances & Components.

The 11 industries reporting contraction in November were: Printing & Related Support Activities; Plastics & Rubber Products; Chemical Products; Paper Products; Transportation Equipment; Fabricated Metal Products; Furniture & Related Products; Machinery; Nonmetallic Mineral Products; Miscellaneous Manufacturing; and Primary Metals.

ISM PMI Respondent Commentary

- “High mortgage rates continue to hamper demand for new housing construction, which is a key market for adhesives and sealants.” [Chemical Products]

- “Business remains slow. We anticipate that the first half of 2025 will be similar and hope that demand increases in the second half of 2025.” [Transportation Equipment]

- “Inflation, even after easing, continues to impact demand. Consumers are looking for value, and purchasing behaviors are changing as many shoppers reduce consumption, causing softer volume.” [Food, Beverage & Tobacco Products]

- “Backlog is rising precipitously after 18 months of troughing. The long-awaited pent-up buying has started. Competition for qualified technical labor is a constraint on operational throughput.” [Computer & Electronic Products]

- “A general construction slowdown in the fourth quarter has created a surplus of finished goods, creating the need for an extra two weeks of shutdown over the Christmas holiday period. We are carefully watching demand in the first quarter to determine if more permanent workforce reductions will be necessary.” [Machinery]

- “Business is slowing as customers destock and appear uncertain about near-term demand. Preliminary forecast for 2025 is down significantly; we hope to see improvements now that we are beyond U.S. election uncertainties.” [Fabricated Metal Products]

- “Our supplier has a positive outlook on the U.S. economy going into 2025. Our business is seeing an uptick in sales forecasts for the first quarter of 2025 versus the fourth quarter of 2024. Overall, our outlook for 2025 is optimistic.” [Textile Mills]

- “We’re finally seeing traction in the last few weeks (with) a higher volume of orders. Backlog is starting to grow.” [Electrical Equipment, Appliances & Components]

- “Late to the game, we are now working on our buying plan in light of potential increased tariffs on imports from China. Cost and capacity of U.S. manufacturing is a concern; a lack of relationship with alternate low-cost international manufacturers is another.” [Miscellaneous Manufacturing]

- “After the election, we have seen an uptick in customers wanting to come back to the U.S. for making their products. We are working through these inquiries. They seem very motivated.” [Primary Metals]

Related Posts

-

Despite an August uptick that ended four straight months of decline, the latest reading indicated…

-

Missing economists' expectations of an increase, the latest PMI reading indicated contraction for the 19th…

-

The report indicates continued economic uncertainty as demand weakens and contraction persists across many manufacturing…