After a one-month reprieve, U.S. manufacturing activity fell back into contraction territory during April, according to at least one leading economic indicator.

Released May 1, the Institute for Supply Management’s monthly Manufacturing Purchasing Managers Index (PMI) — widely viewed as a reliable barometer for the health of U.S. manufacturing — returned below its breakeven mark, where it’s been for most of the past two years.

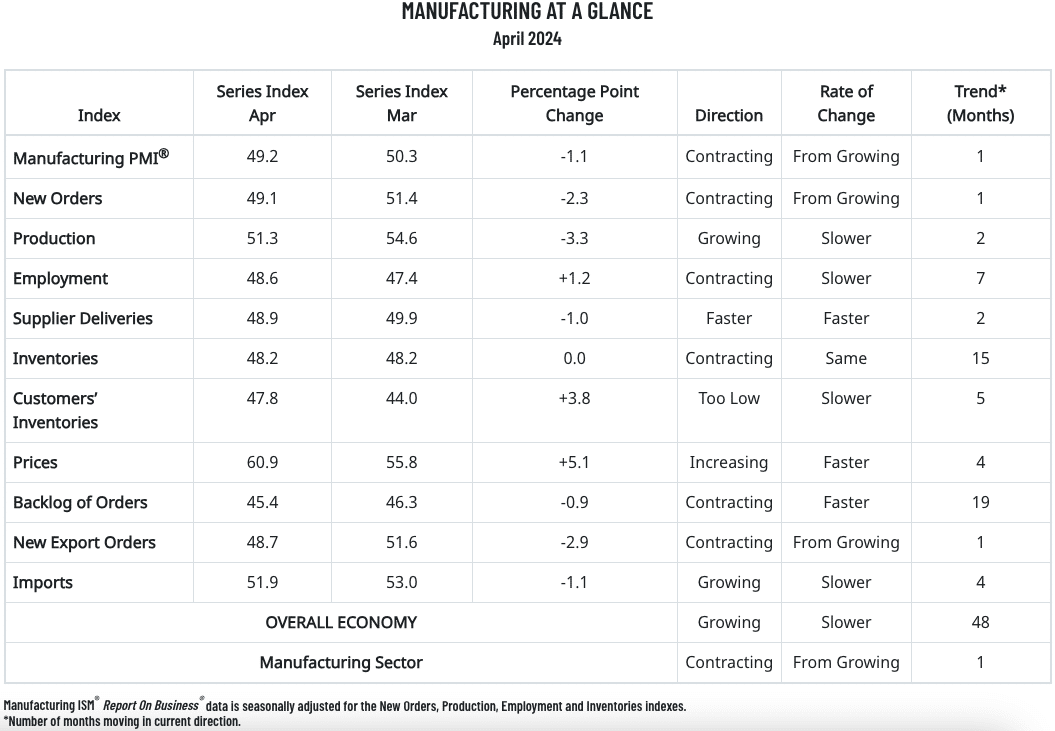

April’s PMI had a reading of 49.2%, down 1.1 percentage points from March, which had been its first reading above 50.0% since September 2022.

Economists surveyed by Reuters had forecast essentially a flat April PMI at 50.0%.

Overall, the latest reading indicated that U.S. manufacturing moved back into contraction territory during March and at a moderate monthly pace.

The PMI’s 10 factoring indexes were led by its index for prices, which moved up 5.1 points from March to 60.9% — its highest reading in nearly 2 years. Meanwhile, the indexes for production fell 3.3 points (to 51.3% and new orders fell 2.3 points (to 49.1%), while customers’ inventories increased 3.8 points (to 47.8%.

“Although demand improvement slowed, output remains positive and inputs stayed accommodative,” ISM Manufacturing Business Survey Committee Chairman Timothy Fiore commented on the April report. “Demand remains at the early stages of recovery, with continuing signs of improving conditions. Production execution continued to expand in March, but at a slower rate of growth than in prior months. Suppliers continue to have capacity but work to improve lead times, due to their raw material supply chain disruptions.”

Of the six biggest manufacturing industries (by GDP contribution) that ISM tracks, two registered growth during April: Transportation Equipment, and Chemical Products. ISM tracks 16 industries overall, and nine registered growth during April. They were, in order: Nonmetallic Mineral Products; Printing & Related Support Activities; Primary Metals; Textile Mills; Electrical Equipment, Appliances & Components; Petroleum & Coal Products; Transportation Equipment; Chemical Products; and Plastics & Rubber Products.

The seven industries reporting contraction in April were, in order: Miscellaneous Manufacturing; Machinery; Furniture & Related Products; Wood Products; Food, Beverage & Tobacco Products; Fabricated Metal Products; and Paper Products.

Survey Commentary

Here is a sampling of PMI survey respondent commentary that ISM provided for April:

- “Conditions are improving as demand is starting to recover. Costs continue to be a major concern as suppliers that rapidly increased prices in the follow-up from COVID-19 are slow to return to pre-pandemic levels.” [Chemical Products]

- “Sales continue to exceed expectations in 2024. The forecasted dip in commercial vehicle production volumes appears to be avoided. Operational output is still strong, and the supply chain has the capacity to support. International supply chain risks have been minimized, but the frequency of supplier insolvencies or bankruptcies appears to be increasing.” [Transportation Equipment]

- “Order flow has stabilized. It took some customers longer to replenish their supply chain network after the fourth-quarter rush we commonly have. Order rates are expected to remain stable through August.” [Food, Beverage & Tobacco Products]

- “Some small indications of market improvement in China for our instruments and technology. Recovery is still slower than we had hoped, and macroeconomic uncertainty remains in Europe and the Middle East, as well as domestically in the U.S. with ongoing inflationary pressures and anticipation for the (upcoming) election.” [Computer & Electronic Products]

- “Market conditions have definitely softened. Thankfully, our backlog is strong and will get us through the year. When conditions improve as expected later this year, we will be in a good position to continue building the business. We are a manufacturer of automated packaging equipment for the food and beverage industry, and with a continued shortage of workers, our customers are requiring more and more automation.” [Machinery]

- “Business is slowing down — it has been a gradual decline for the last several months. We are not seeing new orders at last year’s level, or at this year’s budgeted levels.” [Fabricated Metal Products]

- “There has been a lot of volatility in sales. On average, our sales look flat, but the volatility is concerning.” [Electrical Equipment, Appliances & Components]

- “Business remained strong through the first quarter and has started strong for the second quarter. Commercial construction is still going well but on a regional basis, with the Southeast the strongest.” [Nonmetallic Mineral Products]

- “The major factor affecting our business is the uncertainty of the Federal Reserve’s handling of interest rates, which will affect our customers’ businesses, thereby affecting ours.” [Plastics & Rubber Products]

- “Business is stable, and orders have been consistent. We’re quoting new business for the factory, and automotive builds continue at averages but not near maximum outputs. Workforce is stable, with the turnover ratio dropping considerably. Salaries and hourly rates increasing to meet inflationary pressures.” [Primary Metals]

Related Posts

-

At long last, U.S. manufacturing activity appears to be back in the black.

-

Orders bounced back from a down October for their third gain in four months.

-

It was the third decline in the past four months, and much sharper than December’s.