Author’s Note: This is the third of a three-part series from Waypoint Analytics President Randy MacLean on “How to Exploit Demographics for Growth,” which addresses the labor challenge for distributors, and presents solutions that will put them back on an accelerated growth track for the rest of the decade. (Companies already executing on this are free from constraints and posting record results.) See Part 1 here and Part 2 here.

At WayPoint Analytics, we’ve been providing distributors with turnkey profit analytics for more than fifteen years. This has been guided by executives and experts with inspired insights into what really makes market leaders. Many of these companies convert revenue to bottom line at rates above 15%, and in some cases, get 20% and 25% to the profit line.

This has made these companies practically immune to the labor shortage, as they drive profit rates that fund high wages and great working environments. Nearly every company can do the same, and in this article, I’ll share how it’s being done.

Labor Shortage

Declining birth rates and increasing college education rates have coalesced into a significant labor issue in western countries. The cohort of non-college-educated 20 to 35-year-olds has declined from 31 million in 2000 to 25 million in 2022. This diminishing labor pool is not only the source of our warehouse, delivery and clerical employees, but also shared with construction, manufacturing, hospitality and the military.

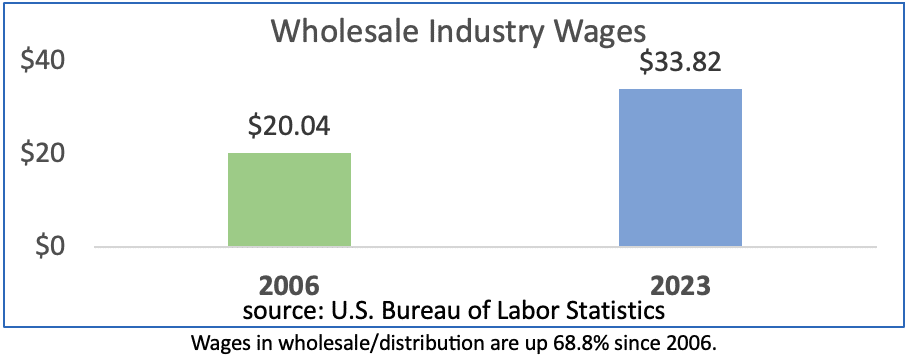

This has driven wages in wholesale/distribution from $22.04 in 2006 to $33.84 in 2023. We’re competing with a host of other employers for a smaller number of people. Turnover is reaching frightening levels.

The outlook is bleak – birthrates dropped below replacement levels more than a decade ago, and this is not going to get better. If this reversed right now, it will be two decades before the newborns enter the workforce.

The Solution (Big Picture)

Simply put, there are three focus areas companies need to adopt – and quickly:

- companies MUST adapt to much-higher, competitive wage rates

- as far as possible, labor must be utilized ONLY where it’s absolutely necessary and contributes to profits, not losses

- higher wages must be funded by gains in customer profit generation

I covered the first two items in detail in parts 1 and 2 of this series. Here in Part 3, I’ll go into depth on the sales side.

To amplify the first of the three points, your company will have to be capable of offering industry-leading (not just industry-matching) wages. You’ll need to obtain and retain the labor needed to serve customers. Turnover needs to be avoided – it reduces your customer-centric focus and absolutely destroys customer service levels.

For the second point, labor will have to be deployed more sparingly, directed to customers and products that drive sufficient profit levels to fund it. Productivity and efficiency measures, combined with detailed cost analysis is needed to know (for sure) if this is being done.

And for the third, detailed customer profitability analysis drives the funding for more competitive wages, and also the deployment of labor to both customer accounts and product categories that provide the new profits needed for funding wage increases.

Finding Balance

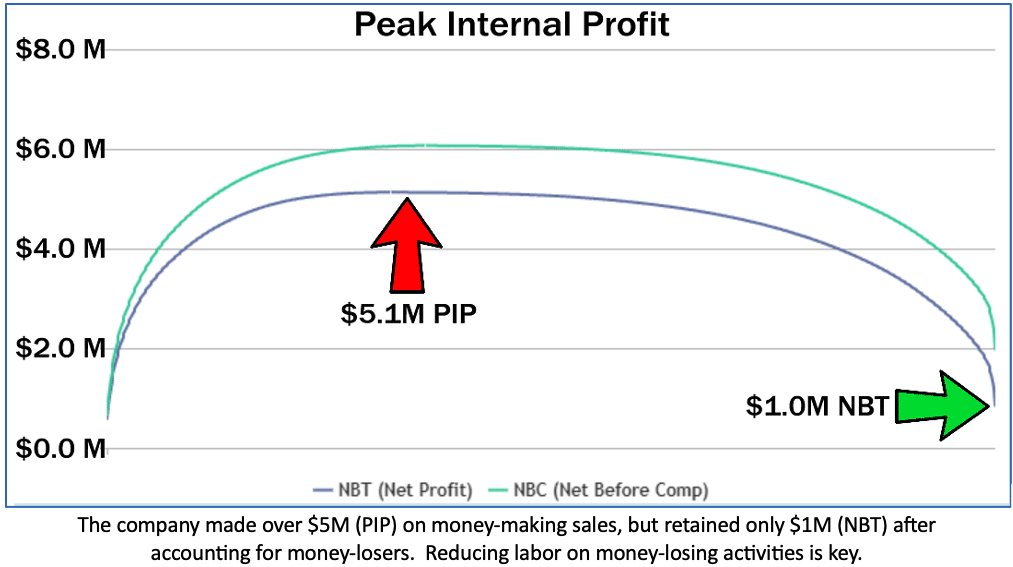

It’s no surprise that customers have differing values to your financial results. The startling realization is the shockingly-high proportion of sales are actively destroying already-made profits. Industry-wide, more than 60% of sales are unprofitable by any measure.

The reason for the difference between PIP (Peak Internal Profit) and NBT (Net Before Taxes, or bottom line) is because most sales are money losers. Let that sink in – more than half of what you write destroys more than half the profits you’ve already made!

In fact, if you get that 60% down to under 50%, you can have industry-leading profit rates. Shifting the balance to more high-conversion, money-making accounts and fewer profit-draining accounts is the only way to drive up cash-flow and profits, and is the key to funding more competitive wages.

What Really Drives Customer Profitability?

Operating profitability is driven by OpCash (“operating cash” or gross profit dollars), driven by volume and margin which represents the ceiling on available profit), less Cost-to-Serve (expenses incurred to service the account).

Most companies have pretty good customer-level information on OpCash (gross profit), and have nothing at measuring customer-level Cost-to-Serve. Without the whole picture, profit management is practically impossible, and initiative effectiveness ranges from disappointing to outright destructive.

Companies cannot excel without accurate and detailed cost analytics.

Customer Profitability Analysis

Most sales lose money, thus cancelling profits already made on profitable ones. This sets the stage for effective action. Shifting the balance between profitable and unprofitable sales is what propels market leaders to the top.

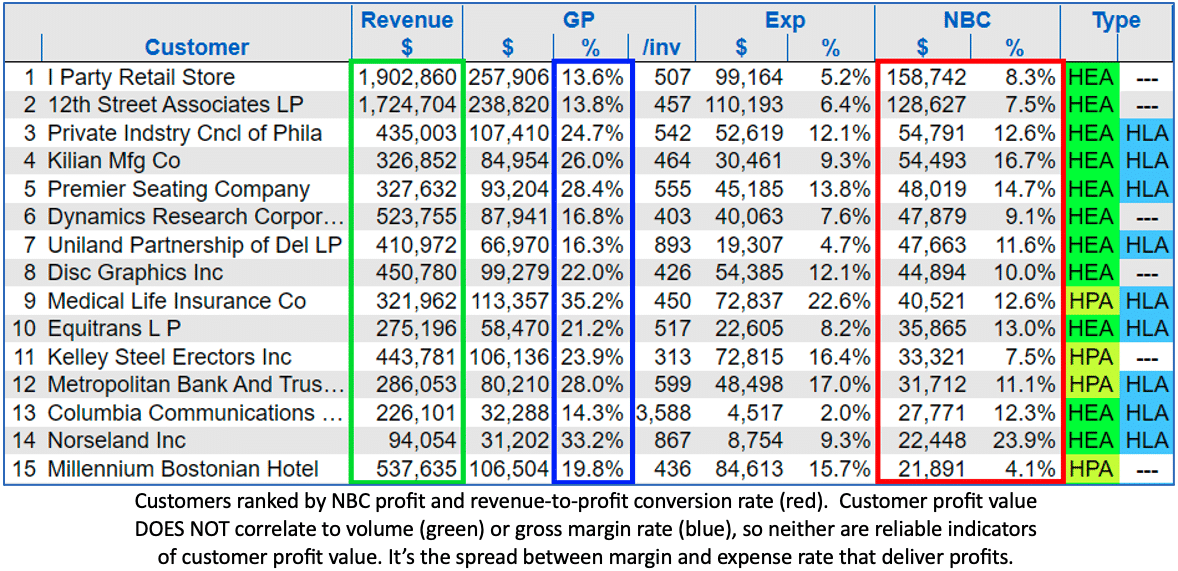

The predominant factor in customer profit generation is individual customer cost-to-serve (or expense) rate. It’s useless to apply a generalized expense rate to known customer margins. Statistically, the average rate will not match over 96% of sales, and will be off by a mile on those where it really counts. (Check the extreme variability in customer expense rates in the example below.)

This why detailed customer cost analysis has been a priority for the market leaders. Knowing where profits come from (and where they’re lost) is necessary for effective profit management. Let’s take a look…(Click on the chart to open a hi-resolution version.)

Gross margin rates are not correlated in any useful way to customer profitability or customer value, yet it’s the predominant (and highly dysfunctional) metric most distributors still use to evaluate sales value. In the profit ranking above, neither sales volume nor gross margin rate will identify the top five accounts.

No operating company would have accounting that didn’t include expenses, but almost all distributors run their sales strategy and activities with gross margin alone, not accounting for expenses at all.

New Metrics

With detailed analytics, strategy and decision-making are driven by NBC (operating profit) and NBC conversion rate (conversion rate of revenue to profit). These are the two columns in the red block in the table above.

NBC dollars show the exact value of the account – what does the customer relationship deliver to the bottom line, and NBC % rate indicates the efficiency of the account in converting revenue to profit. Clearly, a customer with over 20% of the revenue getting to the profit line represent a much greater opportunity than a typical one at 3.5%. The former generates more than five times the profit for each new dollar in sales.

Each account has its own cost envelope, with particular costs depending on order size, ticket lines, direct/warehouse sales type, delivery cost, commission rate, rebates and a myriad of other factors. This is reflected in the Exp % column, which indicates the percentage of revenue that is consumed in servicing the account. Knowing expense rate is essential to managing profits, to delivering funding for higher wages, and is a key output of robust profit analytics.

Clearly, a customer that requires only 10% of revenue to handle their product represents a greater opportunity than one where 30% of revenue is consumed.

Cash flow and profits (NBC) are directly delivered by the spread between gross margin rate (GP%) and the expense rate (Exp %).

We use these metrics to do detailed customer segmentation, identifying accounts where:

- sales penetration activities will drive more cash-flow;

- account protection and customer loyalty programs will retain high efficiency accounts;

- where policy changes and revenue enhancement programs can generate new profits;

- where lean services can make them more profitable;

- and more.

How to Fund Higher Wages

There are a number of well-known, widely-applied sales activities, but a scattershot application is largely ineffectual or counter-productive. (It’s not helpful to successfully acquire more money-losing accounts, or reduce service levels on highly-profitable ones just because they have lower volumes, or to increase prices on low-margin accounts that are already profitable.)

To fund higher wage rates, we need new cash-flow, and there are several highly-reliable ways to get it:

- Penetration Selling – Identify HLAs (High-Leverage Accounts, blue blocks in the example)) as those with the highest revenue-to-profit conversion rates. An account that converts revenue at a 20% rate will deliver four times as much for each new sales dollar as another with a 5% rate. And since the truck is already going there, incremental sales don’t have all the incremental costs, raising the overall rate for everything sold to the account. Focus sales effort on finding more products that these accounts can buy.

- Customer Growth Programs – HEAs (High Efficiency Accounts, green blocks in the example) can be profitable with reduced pricing in targeted cases. Help these accounts grow by assisting with special pricing on large bids. Knowing their expense rates ensures you price the special bids to be profitable. Growing their business grows your business, and creates true loyalty. Create an organized program to facilitate this, and add new cash flow.

- Order Efficiency Improvements – All accounts generating above-average OpCash (gross profit) can have reduced manpower requirements and reduced cost envelopes with reductions in order frequency. For example, daily orders could be changed to Tuesday/Friday. Similarly, VMI (Vendor Managed Inventory) programs can put an inventory of low-value items on the customer’s floor, with periodic replenishment. These practices reduce manpower requirements and free up cash-flow for wages.

- Adjust Cost Structures – “Regular” accounts (those that represent annual gross profit dollar values below the company’s average) can generate more free cash-flow by eliminating certain costs and manpower. Ideally, they would not qualify for: trade credit (cash/check/credit card only); sales commissions; free delivery; free installation; etc.

- Charge for Services – Consider delivery as a product, and sell it at a markup. Recognize both its cost and its value, and price accordingly. Even if you do not recover the entire cost of delivery, a small fee still contributes to new cash-flow. Apply the same logic to other value-added services you provide.

- Rebates – Manufacturers drive their sales volumes and customer loyalty with rebate programs that add new money to your operations. Exploit this by actively working to shift sales into lines that have rebates available. Also work to increase the frequency of rebate payments – don’t wait for up to a year to get the rebates you’ve earned. Most suppliers have quarterly (and even monthly) cycles available, and this is one of areas where large players get an advantage over you.

- Direct Sales – Wherever possible, offload logistics costs and manpower to suppliers by arranging direct sales. You can offer slightly reduced pricing so you can win additional business, but be very careful – distributors are prone to over-estimating savings and then underpricing. Profit should increase on these sales.

- Utilize Analytics – Ensure you target initiatives where they’ll actually work and will drive the largest gains. Even very sensible ideas will not achieve anything in areas that are already optimized, or where the level of activity the initiative addresses is low. Worse still, applying these ideas blindly will most often hurt profits, so be sure you have the information to target the right areas.

Get immediate gains by going after the high-return areas, and monitor the results into the future to make sure the gains aren’t lost as new practices revert to prior methods.

Find Out How Much Potential You Have

In wholesale distribution, over 62% of orders lose money, and companies retain only 27% of their Peak Internal Profit (see the whale curve above). This means that a doubling of bottom-line profit rate is easily achievable.

To help executives get a grasp on how much extra profit is likely available (it’s a lot), and where they’ll most likely get fast results, we’ve created an online assessment system to privately see how their company is doing.

The Distribution Performance Assessment is a secure online system that compares your company to the industry, and also to the front-runners. Combining your numbers with more than $100B of industry history, it also presents pretty good estimates of your performance on critical internal measures used by the industry leaders. It delivers a customized confidential report in about three minutes.

The system is available to industry executives at no charge and can be viewed here. You can see a sample report on the site.

Conclusion

The actions from part 2 of this series create an operational environment where the need for labor is reduced and, more importantly, make all sales incrementally more profitable.

The practices laid out in this part capitalize on operational efficiency, and generate new cash-flow that will fund higher staff wages and boost the company’s profit rates. Many of these actions are highly dependent on targeting from accurate cost and profit analysis, and so I highly recommend you have a robust analytics capability.

In the current day, these ideas are already important for maintaining or restoring profitability. Going forward, they’re a requirement for long-term survival in the new labor environment. I hope you and your team will get an early start with these ideas, and post record financial performance in the coming year.

If you’d like to know more, or discuss some of the ideas in this series, I’d be delighted to talk to you.

The Labor Demographics Series:

Be sure to check out the rest of this series:

Part 1: How Changing Demographics are Killing Profits

Part 2: How to Apply Analytics for Smarter Distribution Labor